Holding the line

Market bouncebacks aren't always on time.

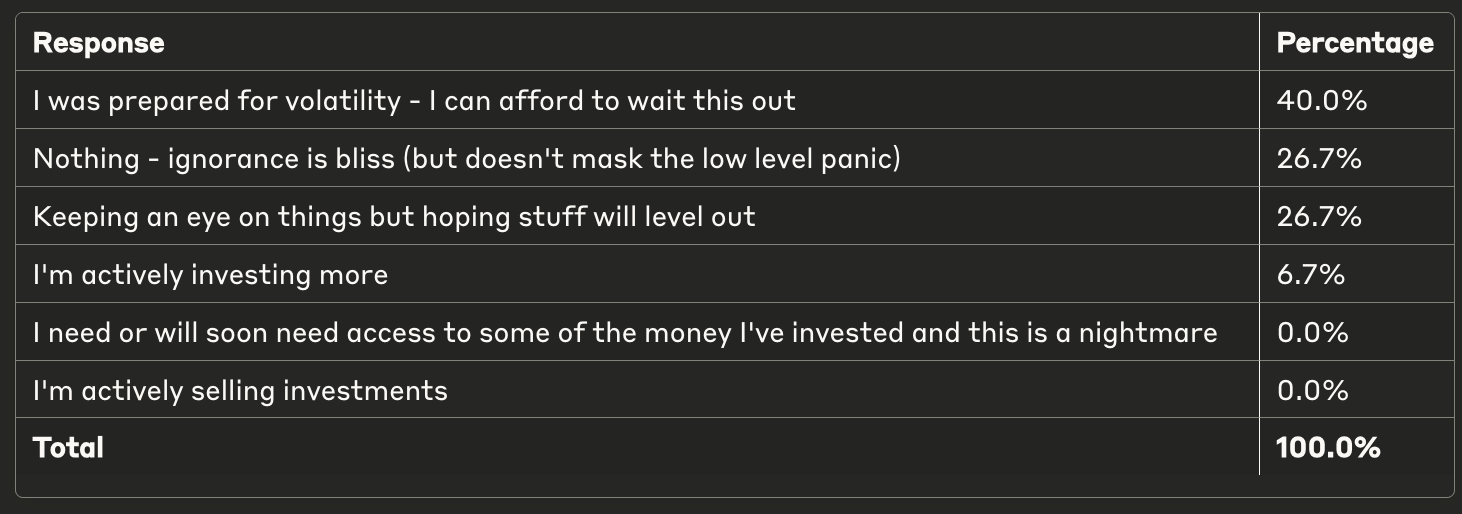

We ran a little poll in the WhatsApp group this week, to see how people were reacting (in terms of action, not vibes) to what’s going on:

I would be fascinated to investigate this further with a wider group of people, and segment the data based on age and risk appetite.

Age is particularly massive; it’s why people’s pensions and 401ks are making the headlines. People who are reliant on these investment vehicles don’t have the luxury of time to wait for values to go back up. They need this money now or will start needing it very soon. They’ve spent decades waiting already.

As one person in our group said, “We usually just ride the waves knowing we have time for it go back up.” But this time, there isn’t the time.

Her ideas for what individuals can take include the following:

Check your portfolio mix: Make sure you know how much of your investments are in stocks, bonds, and other assets. Consider diversifying abroad. Make sure you understand any ETFs or mutual funds that you hold. Holding some mix of equities, cash, different bond maturities, or even other assets (like real estate) can help balance risks.

Cash reserve: If markets get rocky, having a few months of expenses in cash (or something very close to cash) is a good cushion. It keeps you from being forced to sell investments at a bad time.

High yield savings account: If you’re risk‐averse, stick it in a HYSA. You’ll earn a yield and can exit fairly quickly if needed. I have about half my portfolio in this.

Don’t panic sell: Headlines can sound frightening, but panicked selling rarely helps. If you have a diversified, long-term portfolio, short-term volatility is often just noise.

1. UK taxpayers warned to be diligent over savings interest or face fines

You have to pay tax on interest earned from savings over a certain threshold (depending on your income tax level).

And, even though it’s your job to keep on top of this, and declare and pay anything you owe, HMRC can play a role in this too.

HMRC receives information directly from banks and building societies on people’s savings interest. And it’s said it will use this information to calculate any tax due and contact taxpayers directly.

But it’s unable to match one in five accounts to a taxpayer record. So if you think you might be affected, do the maths and then contact HMRC.

If there’s a delay in doing so, you’re still liable to pay penalties (failure to notify penalties, late filing penalties, late payment penalties and late payment interest). The late payment interest rate is currently 8.5%.

2. UK mortgage lenders cut rates after the tariffs

I got Claude to explain this, as I was struggling to fully understand why high interest rates in the US would allow UK interest rates to go lower.

Here’s what it came up with:

The UK, like many countries, has been dealing with inflation (high prices) for some time. To fight inflation, the Bank of England has kept interest rates high. High interest rates help slow down price increases by making it more expensive to borrow money, which reduces spending.

Now, here's how America's high tariffs create an opportunity for the UK:

When Trump puts high tariffs on imports to America, this likely causes higher inflation in America.

To fight this inflation, America will probably keep its interest rates high.

The UK usually has to be careful about lowering its interest rates before America does, because if the UK's rates are much lower than America's, this can cause problems for the British pound and the UK economy (because money is going to flow to the US, where investors can earn more money via interest, and far less will be invested in the UK).

But in this case, if America is keeping its rates high specifically because of tariff-related inflation (which doesn't affect the UK), the UK might have more freedom to lower its own rates.

This is because the reasons for high interest rates would now be different in each country - America's high rates would be responding to tariff-related inflation, while the UK's normal inflation might be improving.

So the UK could potentially lower its interest rates sooner than it originally planned, without worrying as much about the usual problems that come from having rates much lower than America's.

When the UK lowers its interest rates, mortgages become cheaper, which helps more people buy homes - and that's how it could help the UK housing market.

3. The cheapest a funeral can be is £1,395

Some people can’t afford flowers for a funeral. To the point that those who can are asked if they want to donate theirs to someone else, after the ceremony.

And everything in a funeral costs money. £49 for a set of 10 slides (but you have to adhere to strict time automations; 10 seconds a slide). You can get fined for running over time.

The writer of this piece ends up opting to go for a memorial service, and a direct cremation instead. “Without the presence of a coffin you are free to do what you want, where you want, when you want.”

But you need family permission. Says the undertaker, “It’s amazing how many families can’t afford a funeral but have to do the whole works because other family members insist.”

This is one of the reasons it’s important to think about your wishes and include them in a will. If you want a traditional funeral, specify it (and perhaps consider setting aside money for it). If you want something else, say!

Links!

Money

Barclays begins paying up to £100 compensation to customers after banking outage

Easter is getting the Easter treatment in the UK; trees, decorations and gifts such as sheep jumpers and bunny-shaped trinkets are a distraction from the gloom

Spending on luxury weddings is booming

I liked this money saving tip from

Life

SNL is coming to the UK (on Sky). Will be interesting…

We basically need an AI Pearl Harbor before people will take [the dangers] seriously. Also, apparently Claude is “the chatbot of choice for a crowd of savvy tech insiders” 😏

Fascism thrives on women’s self-doubt oooof

There probably won’t be a newsletter next week. But there might be a reader survey instead… 👀

Thank you for reading this!