Let's talk about money, I guess

"It's easier to be physically intimate than 'money intimate'."

A few newsletters ago, I shared some research about money and relationships. The headline? A quarter of Brits (in relationships) hide savings from their partners. This made the Money Brunch WhatsApp group pop OFF, which made it an easy choice of topic for January’s in-person session. This is a longer piece informed by those discussions, which exclusively happened to centre on female-male relationships.

There’s a plethora of things to explore in the intersection between money and relationships — and a lot of it can centre on spending. Like: Is it OK to not split the bill on a date? How do women ‘earn back’ the financial investment they’ve made into their appearance? Is it anti-feminist to ask your boyfriend to pay your rent?

In our recent discussion, we looked at broader issues:

What financial information — and access — do you open up to your partner, and when?

Does a lack of full transparency and access mean that there’s a lack of trust, and therefore, that the relationship won’t be successful?

Do women think about money differently in relationships, compared with men?

What’s mine is yours?

In simpler times, when two young people (with little to no wealth or debt) decided to get married, ‘what’s mine is yours’ was an easy maxim to follow.

Once you’re in the relationship, you’d be working exclusively towards shared goals. Typically this would involve one person ‘bringing home the bacon’ and one person doing pretty much everything else required to make a home, family and life work. While the second person is on the clock all the time, they aren’t building up any financial resources. They’re entirely financially dependent on the breadwinner.

That, of course, typically leads to women not being protected. One of the reasons I do this work is because I’ve spoken to SO many women who took that approach. But who, after divorce, found themselves later in life at a massive financial disadvantage — wishing they had taken the time and effort to invest in financial literacy and management.

Money is intrinsically linked with agency and freedom. It’s no surprise that people are more guarded going into relationships nowadays. Men (and society) may view women as gold diggers. But women are typically opening up a more cavernous reservoir of love, care and support - and this isn’t something you can account for in a pre-nup.

Add to that the opportunity cost of missing out on earnings, when taking on additional caring duties, having children, and even ‘prioritising their relationship. And this inequity is further compounded when you think about them bringing their financial assets into the relationship too.

As one Money Bruncher said, ‘Women need to set more boundaries because they give more.”

A fair share

Having your own finances can act as an insurance policy if things go south in the relationship. Someone shared a story about a man changing in their relationship as soon as they got married, and having strong (previously unseen) views on women as property. Someone shared how their ex’s family started to have a stronger influence over him, and also pressuring her to being in her family’s wealth into their joint assets, and the relationship ultimately broke down. She ended up spending £40k on getting divorced (draining her savings); this would have been even higher had the case gone to court.

There’s also the concept of having a F*ck Off Fund; an escape hatch that lets you get out of situation you may otherwise be trapped in — like an awful job, or an abusive relationship.

When two people come into a relationship on unequal financial footing, it’s going to be a longer journey to reach a point of balance.

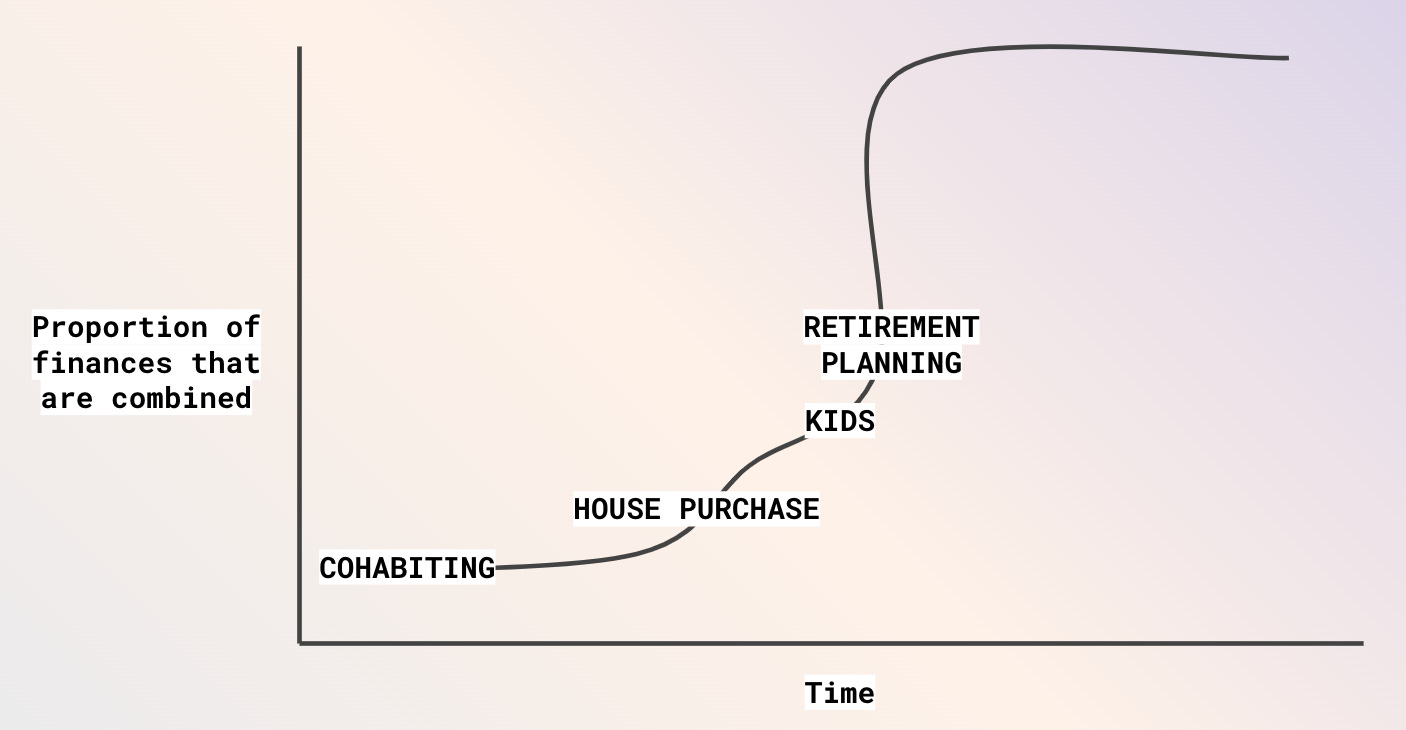

Typically, couples take a more phased approach to sharing finances, opening up access to money over time. It might start with a shared expense account for shared expenses when cohabiting, increasing when buying a property together, and then increasing further when having kids.

This graph illustrates how this can play out.

Things get interesting when retirement planning comes into the mix. If you’re planning on spending your retirement with the other person, that’s the point at which it’s likely going to become harder to keep your finances separate. A small part may still be kept separate, but broadly, you’re likely to be combining most of your finances and making joint decisions about how to balance managing your investments, and drawing down income.

Why? In retirement, you’re getting income from assets you keep invested (like pensions, and general investments, and potentially, property — likely supplemented by a state pension). And you generate income from invested assets. The larger the asset base, the more income you can generate. Which is why it makes more sense to pool these assets.

Also, retirement planning is complicated. Having someone as invested in making decisions as you are is going to help you navigate these choppy waters.

Ultimately, a relationship’s health isn’t measured by how combined your finances are.

You can’t afford to not do due diligence

Non-casual dating is hard, and one of the reasons might be because you’re doing two things at once:

Figuring out if you like the person (HARD)

Figuring out if you could build a life together (VERY HARD)

On the first point, I’ve got nothing. But, on the second point, there are a bunch of things you can do.

What’s important to you? Are you addressing these things with them — or are you just hoping for the best?

One of our group has a list of questions in her Notes app, which she adds to over time. These questions allow you to assess a prospective partner’s ideas, values and actions (and how they might have changed based on past experiences). And they also help you to see how they might respond to hypothetical scenarios that bring finances into the equation (e.g. If one of your parents required care, how would you approach this? / If you got really sick and were unable to work, how would you support yourself, how would you cope?).

This is the un-romantic side of dating. It’s a drawn-out interview process, with a series of interview questions and small tests.

You also want to make sure that you’re collecting hard data based on what they do, rather than what they say.

Meet their friends and family, and observe them in their natural environment. Someone talked about the importance of being with their partner in social gatherings and networking events, and seeing how they act.

We do so much work in painting a picture of someone based on inferences we’re making about them, and this is especially easy to do with digital communication (messages, social media likes, emoji reactions). It’s far more valuable to collect ‘primary data.’

As one person put it: “Down-weight messages and calls. Spending time together is how you figure this stuff out.”

Deal-breakers don’t magically disappear

One person shared a situation in which a couple had diametrically opposing views on finances. The woman spelled out what they wanted in order for the relationship to change, but allowed it to continue for four years. The relationship eventually ended.

If there’s a deal-breaker, and you’ve discussed this and they’ve agreed to address this, you must give them a timeline to do so and hold them accountable.

Another person in the group said they’d have set a clear two month timeline for this change to happen. And then later said they’d actually have made it a month, but were trying to be a bit more diplomatic.

There are times when change is possible, and others when it really isn’t. Part of the work in relationships is working that out. “A tiger doesn’t change its stripes.”

How are you making room for change?

The human experience requires people to change. This means that someone’s view on something is not given as fixed. And in a healthy relationship, there’s space for both people to evolve.

Therefore, regularly checking in and questioning both of your values and goals is critical.

One person talked about an AGM she had with her partner. It started out as a joke, but actually became incredibly helpful for providing a dedicated space in which to reflect on their goals and values, and how they wanted to spend time and energy on in the coming year.

As someone for whom using corporate vocabulary in everyday life is second nature, I loved this. See also: Monthly and quarterly reviews; quarterly and annual planning; budget setting.

There’s also a world in which your relationship runs its course. And it would be foolish to completely write this off as a possibility. It doesn’t mean that you believe that’s likely to happen, and that you’ve sabotaged the relationship. It’s just a pragmatic way of looking at things. After all, no-one knows what the future holds.

It’s not sexy to talk about money

There are two things going on here.

Firstly, physical intimacy can come far more easily than financial intimacy. There’s a reason why money is widely regarded to be the last taboo.

And, secondly, talking about money and proactively shaping your life is arguably ‘unfeminine.’ That’s years of conditioning and expectation about women being passive and demure for us to work with, and deconstruct. In some aspects, it can be easy to ask challenging questions. But asking someone how much they earn, and what their wealth and debt look like? That’s a harder conversation to bring up, if only because it’s uncomfortable.

There’s a lot of discourse about how men say they want a strong woman, but when push comes to shove, they are more comfortable with someone who conforms to traditional gender roles. And, perhaps, the same is true of women too. At least in this case, there’s a playbook to follow. One in which money talk is swept under the rug.

Trust your intuition

Trust is the key to a healthy relationship. And that includes trusting yourself.

You need to be attuned to what’s important to you. This involves thinking about the role you would like to play in a relationship, and what you’d like from a partner. Part of this includes defining your views towards finances. Just as you are asking a prospective partner about hypothetical scenarios, so too you need to do the same for yourself. This needs to be a continual process; it’s not a one-off exercise (see above point about change).

This leads to a stronger set of instincts. If you’ve been keeping your finances entirely separate, but now you feel as though you might want to combine them more, look into the why and how. If you have a sense that your partner is concealing something from you, probe that. If something doesn’t feel right, explore that.

I love you, but I love me more

The idea of a perfectly equal relationship, immune to any seismic shift, is dreamy. But the reality is that it’s just that. A dream.

Heartbreak you can (generally) come back from. I’m not saying it’s easy, but that with time and work, it’s possible. Financial devastation, since it permeates every aspect of your life, is a lot harder.

You’re not setting your relationship up for failure if you’re cognisant of the need to protect yourself. No one goes into a committed relationship expecting it to fail. But we all know stories of broken engagements, divorces and custody battles. So it would be foolish to be blind to the possibility.

Addressing finances head on, continually interrogating how you feel about money in your relationship — and laying it bare— is the only logical approach.

Happy Valentine’s Day.