Systems won't save you

Plus, interest rate news, the Bank of Mum and Dad, and real-life redundancy and finance stories.

I’ve spent some time in the world of productivity writing and thinking. OK, a lot. Atomic Habits, Deep Work, The 7 Habits of Highly Effective People… I’ve read them all — and more. I used to think that if I found the right system, a life of juggling competing priorities would fall into a seamless dance, free of any stress or worries.

Of course, that’s not how it actually works. These books appeal because they claim to offer a solution to the mess that is white-collar work, where there’s always far more to do than time there is to do it.

They don’t address any of the structural issues (like how to measure employee productivity in a non-manufacturing world, or how to keep employees afloat when headcount gets slashed — and deliverables remain unchanged).

I was reminded of this ‘system first, processes second’ approach when I had to go into Apple this week. Upon entering, you’re seduced by products that can solve problems that you either have, or think you might have.

I’m not a visual artist or designer but, for a moment, I was tempted to buy the new iPad with the Apple Pencil.

After all, if I had these products, wouldn’t I become a better artist?

The answer is obviously no. In order for this to happen, I’d have to find corresponding time to invest in learning and practicing the craft. Over a long period of time. That’s a FAR harder task than tapping a card to buy, setting up the device and then hoping for the skills to materialise.

Apple is precision-engineered to tip consumers into buying. And that’s what marketing does for us; it sells really compelling solutions — and then leaves it for us to figure out that we simply don’t have the time and/or energy to realise the benefits. And this is expensive!

Once you step through the looking glass, and see this with new eyes, it becomes somewhat easier to build a shield against the onslaught of marketing tactics companies use against us. Easier, mind. Not always easy.

Productivity books still have a place in my life; specifically in my pre-sleep routine; I like to have a little read before going to sleep(!).1 But once you accept that reading them won’t change your life, you too can find them enjoyable.

1. There’s been a UK interest rate cut - but US rates stay unchanged

The Bank of England has cut the UK central bank interest rate by 0.25%, bringing it to 4.25%.

It was a pretty divided decision; of the Monetary Policy Committee (which makes this call) “five [members'] voted to cut rates to 4.25%, two voted in favour of a larger reduction to 4% and two voted for no change.”

It hasn’t been this divided for a while, reflecting how chaotic our current economic (and political2) situations are.

What does this mean for your mortgage and bank interest rates? Rates were already starting to track downwards, since it’s been widely expected that the central bank rate is going to keep going down slowly. So lock in savings rates now! And keep an eye out for lower mortgage rates if you’re up for a remortgage, or getting a new mortgage 👀

Across the pond, the US still hasn’t gone into a recession, but the risks of higher inflation and unemployment have increased. So the likelihood of a future cut is also higher. But, honestly, who knows.

Jerome Powell, Fed Chair, certainly doesn’t. He said, ‘It's not at all clear what the appropriate response for monetary policy is at this time ... It's really not at all clear what it is we should do."

Basically they have no idea what the President’s policies are going to be, let alone what they’ll do to different parts of the economy, so staying put for now is the only option.

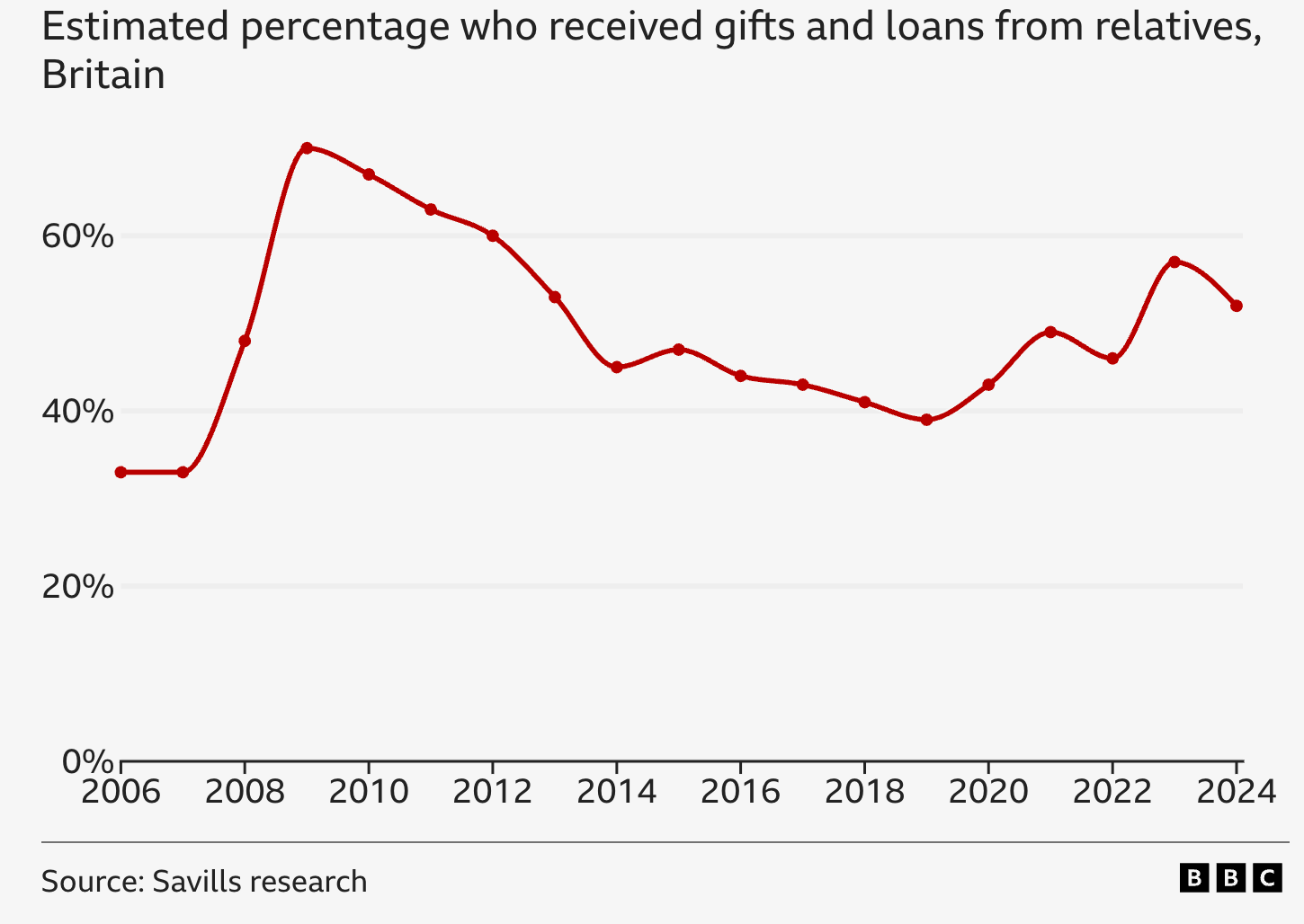

2. More than half of first-time buyers received financial help from their family to make house purchases last year

This figure peaked in 2009 (no surprise, given the economic meltdown at the time), but started tracking upwards again in 2019.

There are two reasons behind this:

Mortgage rates shot up at the end of 2022, following the Liz Truss budget, making them considerably higher than in previous years (and therefore more expensive)

How expensive a mortgage is depends on the size of the loan. If you have a larger deposit, you can get a cheaper loan (this is known as the loan-to-value (LTV) figure). Adding family money to your own deposit savings increases the deposit, reduces the LTV, and lowers the overall financial burden

It’s likely that these numbers will continue to head upwards; we know that the cost of living is getting higher, earnings are not keeping pace, and the ability to save is getting harder.

People are also being incentivised to start distributing some of their wealth throughout their lifetimes, to minimise the future inheritance tax liability on their estates; the Bank of Mum and Dad is also supported by other family members (but the Bank of Mum and Dad and Grandparents and Maybe Wealthy Aunts and Uncles Too is not so catchy).

3. Seven women on how they got through redundancy financially

This is such an interesting read, because you get to see how different people have navigated being made redundant — and they’re open about the finances that drove their lifestyles and decision-making.

The 24 year-old who has been made redundant three times — and put her severance money into a high interest savings account, and Vanguard ETF, while slashing her expenses and taking on part-time work to fund the present.

The 43 year-old who was made redundant soon after buying her first property, surviving on a generous payout to stay afloat, while also slashing her expenses. More recently, she’s been made redundant again. “My mum, who brought me up as a single parent, always said that you need to have enough money for three months in the bank to survive at all times.” This advice has helped her this time around.

The 32 year-old who was made redundant after becoming newly single, and a sole homeowner. She eventually got back on her feet, but admits she hasn’t built resilience for the future: “I don’t think I have learnt from my lessons as I still don’t have the three months worth of savings you should have for a rainy day, and I often feel a bit silly that I spend my money enjoying life. I have it as one of my goals to build my savings back up over time and start being sensible.”

If you like this kind of content, Laid Off by

has way more redundancy interviews, although less money-centric.Links!

Money

A must read.

on the friction economy. “The more we optimize individual experiences for frictionlessness, the more collectively dysfunctional our systems become.”A fifth of people say they avoid checking their bank balance to reduce their anxiety. But this increases their risk of falling into a cycle of debt.

More than half of homeowners are ‘improving rather than moving’ as costs get spicier. Those living in London, Manchester and Edinburgh (expensive places to live anyway) are most likely to do some sort of renovation, compared to those living in Sheffield, Liverpool or Belfast, who are more likely to move.

The single tax persists; single pensioners need £225,000 more in their pension pot than couples to achieve a ‘moderate’ standard of living in their golden years.

Famous people and bad money stories. The one the stands out? “In the late 1990s Leonard Cohen was living in a Buddhist monastery high up on a California mountain. He’d saved something like $5 million for retirement… one day he came down the mountain and put his card into an ATM and nothing came out. His manager had embezzled his life savings!” Don’t trust someone else with your money!

Life

21 observations from people watching - this is both beautifully written and insightful

What happens when your boyfriend gets ‘red-pilled?’ Answer: It’s not great 😕

“Now I look into it, the conditions aren’t that great, and the pay we get is not relative to profits that the company makes.” Trying to unionise at Apple in the UK is hard.

Reaction times using screens while driving are worse than being drunk or high — finally, car makers are going to have to stop making everything touch screen. It’s actually wild that this has gone unchecked for so long.

Sybil Shainwald, lawyer and women’s health activist, has died just short of 97. I’d never heard of her before reading this obituary. She took on pharmaceutical companies “on behalf of women who had been irreparably damaged by ill-tested [contraceptive] drugs and devices.” What a woman.

Finally, Warren Buffet (renowned ‘oracle’ of investing) retired this week, making big news. He made his money in a VERY different world, and also had access to cheap capital. But two key pieces of his ‘evergreen’ advice remain strong and relevant:

Be patient, and wait for a fair price. Don’t buy into companies when the price is high; wait for it to come down (and hope it comes down!)

Hold for the long term. A famous Buffetism is, “if you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.”

PS THANK YOU to everyone who completed the reader survey! Changes are coming 🫶

Substack tells me to put this sharing button in even though I don’t think it’s very effective. But still, I will obey.

They’re easy-to-read, and soothing.

HONESTLY, now India and Pakistan too? 🙄